Artificial Intelligence in Banking: Operational Excellence, Trust, and the New Institutional Mandate

Artificial intelligence is rapidly redefining operational efficiency in banking. From credit risk modelling to fraud detection and customer personalisation, AI systems are increasingly embedded into the core decision-making architecture of financial institutions.

Yet the central challenge facing banks today is not technological capability. It is institutional accountability.

As AI-driven systems influence lending decisions, compliance monitoring, and financial risk assessments, the traditional boundaries of responsibility begin to blur. When algorithms optimise outcomes, who ultimately owns the consequences? When automation scales decisions, how does governance scale oversight?

For banking institutions, operational excellence can no longer be measured purely in terms of speed, cost efficiency, or predictive accuracy. It must also be evaluated through the lens of trust — a foundational asset in the financial sector.

Trust in banking is not built solely on performance metrics. It is sustained through transparent governance, ethical accountability, and leadership clarity. As AI becomes more deeply integrated into institutional processes, boards and executive leadership must redefine what oversight means in an algorithmic environment.

The new institutional mandate is clear: efficiency without governance is fragility.

Banks that succeed in this next phase of digital transformation will not be those that adopt AI fastest, but those that embed accountability frameworks alongside technological innovation. In an era where automated decisions shape financial futures, the resilience of banking institutions will depend less on computational power and more on governance design.

Artificial intelligence, therefore, is not simply a technology upgrade. It represents a structural shift in how banking institutions must think about operational excellence, trust, and long-term institutional responsibility.

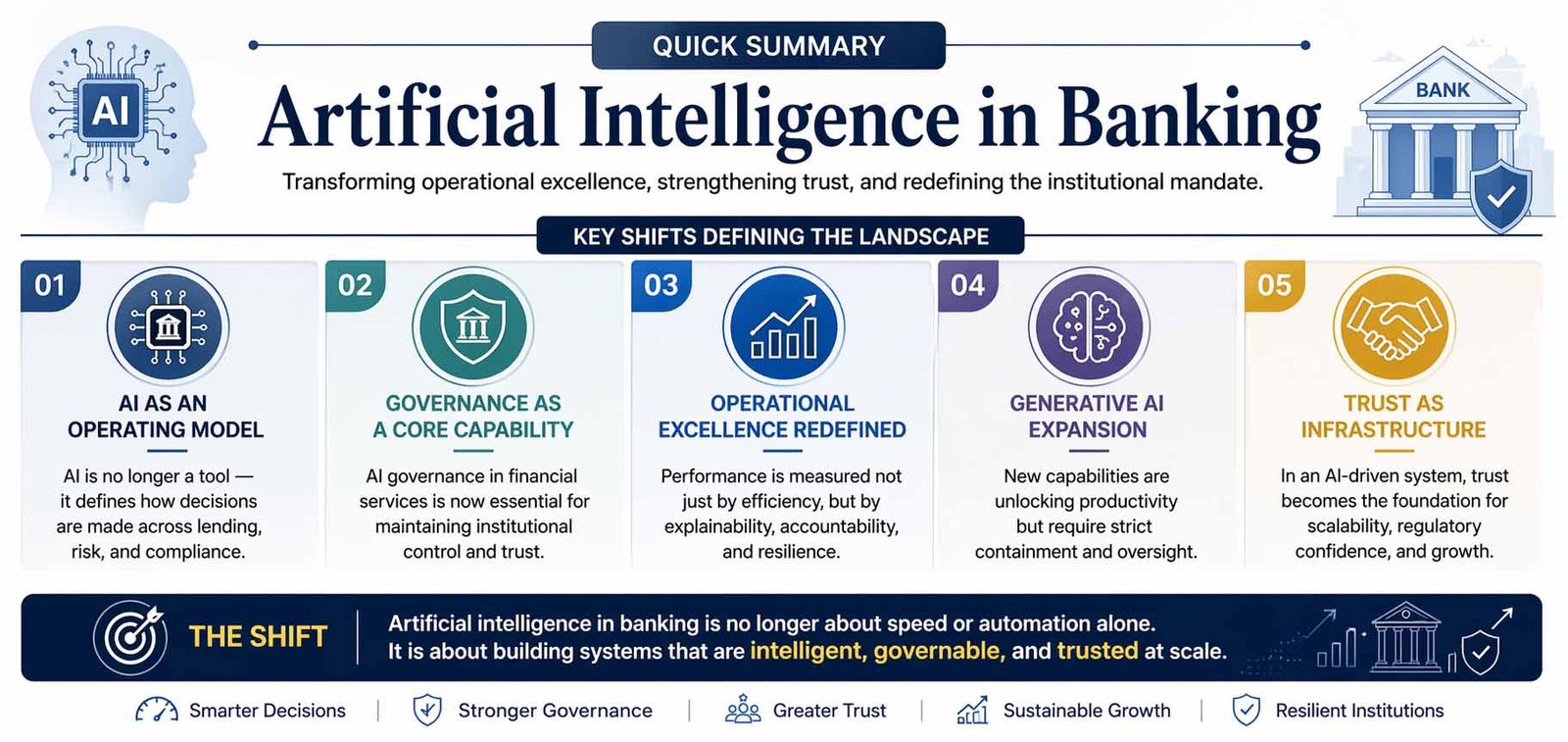

Key shifts defining the landscape:

- AI as an Operating Model: AI is no longer a tool — it defines how decisions are made across lending, risk, and compliance

- Governance as a Core Capability: AI governance in financial services is now essential for maintaining institutional control and trust

- Operational Excellence Redefined: Performance is measured not just by efficiency, but by explainability, accountability, and resilience

- Generative AI Expansion: New capabilities are unlocking productivity but require strict containment and oversight

- Trust as Infrastructure: In an AI-driven system, trust becomes the foundation for scalability, regulatory confidence, and long-term growth

From Digital Transformation to Institutional Redesign

For more than two decades, the technology in the banking industry has been defined by cycles of digitization. Branch networks became digital channels. Paper trails became workflows. Manual reconciliation became automated processing. Each wave was described as progress, and each wave delivered measurable efficiency gains.

But artificial intelligence in banking represents something fundamentally different. It is not merely another layer of digital transformation in the banking industry. It is a structural redesign of how decisions are made, how risks are assessed, and how institutions remain in control under pressure.

Earlier stages of digital transformation focused on improving speed and reducing cost. Today, intelligence itself has become embedded into credit underwriting, fraud detection, liquidity management, compliance monitoring, and customer engagement. Systems no longer simply execute instructions; they interpret patterns, anticipate outcomes, and adjust behavior.

This shift forces a deeper question. If intelligence becomes distributed across systems, what ensures that the institution remains governable? Operational excellence in banking can no longer be measured only by efficiency metrics. This evolution reflects a broader shift within modern Business Excellence frameworks, where governance architecture, institutional resilience, and strategic accountability now define competitive advantage.It must now be measured by how well intelligence is supervised, contained, and aligned with institutional purpose.

The next era of banking will not be defined by who adopts artificial intelligence first. It will be defined by who redesigns their operating model to remain trusted while doing so.

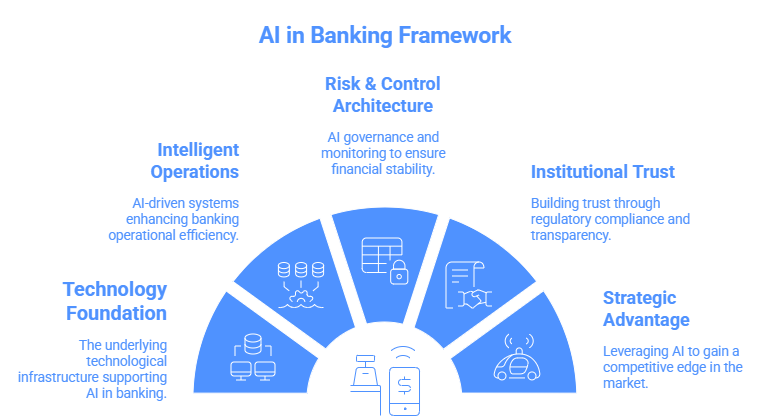

How Artificial Intelligence is Redefining Banking Operating Models

Artificial intelligence in banking is often discussed as a collection of tools. In practice, it is rapidly becoming the architecture of the operating model itself. AI adoption in financial services has moved beyond pilot projects and innovation labs. It now sits inside core processes that determine revenue, risk exposure, and regulatory posture.

Automation in banking operations once meant digitizing repetitive tasks. Today, AI-powered systems shape decision flows. Credit models learn from evolving borrower behavior. Fraud systems adapt in real time to new threat patterns. Compliance monitoring systems flag anomalies before they escalate into regulatory breaches. These systems do not operate at the margins; they define institutional responsiveness.

As AI adoption in financial services accelerates, the distinction between technology and operations dissolves. The operating model becomes intelligence-driven. This creates new forms of scale but also new forms of fragility. A flawed decision can propagate faster than any human review process can contain.

Operational excellence in banking, therefore, must evolve. It is no longer enough to ensure that processes are efficient. Institutions must ensure that their intelligent systems are interpretable, reversible, and accountable. Artificial intelligence in banking demands structural clarity about who controls learning systems and under what conditions they are allowed to act autonomously.

Banks that treat AI as a tool will struggle. Banks that treat AI as an operating principle will redesign themselves accordingly.

Artificial intelligence in banking is abundant. Trust is scarce. The institutions that endure will be the ones designed to remain governable at speed

Digital Transformation in Banking Industry: The Third Wave

The digital transformation in the banking industry has unfolded in distinct waves. The first wave focused on access. Customers gained online portals, mobile applications, and digital onboarding. The second wave focused on efficiency. Back-office processes were automated, and legacy systems were gradually modernized.

The third wave is different. It centers on intelligence. Artificial intelligence in banking now shapes decisions rather than simply facilitating transactions. Credit scoring models incorporate behavioral data. Risk systems use predictive analytics. Treasury functions rely on scenario modeling that updates continuously.

This transformation is subtle but profound. The technology in the banking industry is no longer just infrastructure; it is a decision-making layer. Digital transformation in the banking industry now involves embedding learning systems that evolve over time.

Such systems require a new kind of governance. When intelligence adapts dynamically, oversight must adapt as well. Static review frameworks are insufficient. Supervisors increasingly assess not only outcomes but also how decisions are generated and how risk propagates.

Institutions that understand this shift redesign their architecture around control, not just innovation. Others risk operating intelligent systems without corresponding guardrails. The result is emerging divergence. Some banks will scale confidently. Others will move cautiously, constrained by regulatory friction and internal uncertainty.

The future belongs to those who align digital transformation with institutional governability.

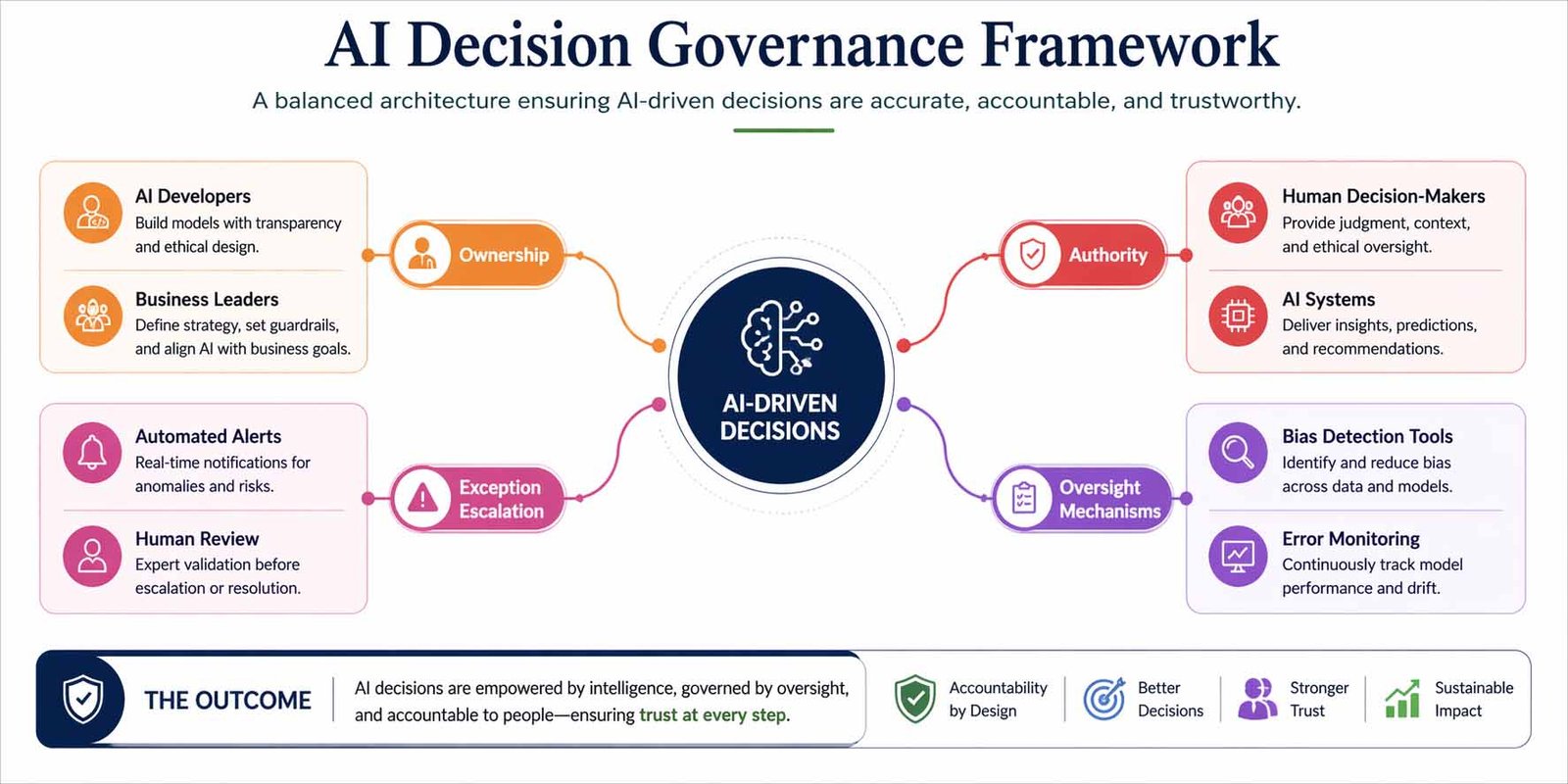

Why AI Governance in Financial Services is Critical for Trust

AI governance in financial services has become the defining capability of modern banking institutions. As artificial intelligence in banking expands across critical functions, the question shifts from whether models are accurate to whether institutions remain in control.

AI risk management in banking extends beyond model validation. It encompasses data lineage, bias monitoring, stress testing, escalation protocols, and decision traceability. When intelligent systems influence lending approvals or compliance decisions, explainable AI in banking becomes essential. Institutions must be able to demonstrate how conclusions were reached, especially under regulatory scrutiny.

Operational excellence in banking now depends on governance architecture. Permissioned autonomy has replaced unrestricted automation. Systems may act independently within defined parameters, but those parameters are explicit, conditional, and revocable.

Explainable AI in banking is not simply a regulatory requirement. It is a confidence signal. Supervisors and stakeholders assess whether intelligent systems can be paused, overridden, or recalibrated without destabilizing the institution.

AI governance in financial services thus becomes the foundation of institutional trust. Banks that embed governance into their operating models signal maturity. Those that retrofit controls after deployment face greater scrutiny and operational friction.

In an environment where intelligence moves at machine speed, governance determines how much freedom an institution is granted to innovate.

Generative AI in Banking: Opportunity and Containment

Generative AI in banking has introduced a new layer of capability. From drafting regulatory reports to summarizing complex customer documentation, generative systems promise efficiency gains and improved responsiveness. Advisory teams experiment with AI-assisted insights. Customer service platforms integrate conversational intelligence.

Yet generative AI in banking also presents distinct risks. Hallucinated outputs, embedded bias, and inadvertent data leakage can undermine credibility. When generative systems influence regulatory communication or financial advice, errors can carry institutional consequences.

Traditional risk frameworks were designed for human-led decisions. AI introduces new layers of complexity — including opacity, model drift, and systemic bias.

Banks must therefore institutionalise:

- Independent model validation processes

- Continuous monitoring of AI systems in production

- Cross-functional governance committees

- Clear reporting structures to boards and regulators

Trust in financial institutions depends not on flawless systems, but on transparent oversight.

AI risk management in banking must therefore expand to address generative models specifically. Containment strategies include structured human oversight, restricted data environments, output validation protocols, and scenario testing under stress conditions.

Artificial intelligence in banking thrives when scaled responsibly. Generative capabilities should augment expertise, not replace judgment. Institutions that treat generative AI as a productivity accelerator without strengthening governance risk damaging hard-earned trust.

The challenge is not whether generative AI in banking will be adopted. It already is. The challenge is ensuring that its integration reinforces, rather than erodes, institutional control.

Operational Excellence in Banking in the Age of Autonomous Systems

Operational excellence in banking once meant minimizing errors and maximizing efficiency. Today, it means something more strategic. It means designing institutions that remain stable while intelligent systems operate at scale.

Automation in banking operations has advanced to the point where systems can identify anomalies, initiate remediation, and escalate exceptions without manual intervention. But autonomy must be permissioned. Systems should know when to defer to human judgment and when to halt activity under stress.

Explainable AI in banking supports this model by ensuring that automated decisions can be traced and audited. Continuous assurance replaces periodic review. Institutions monitor system performance in real time, adjusting thresholds and constraints dynamically.

Operational excellence in banking now combines efficiency with resilience. It is measured by how effectively a bank absorbs shocks, contains risk propagation, and maintains transparency under pressure.

Artificial intelligence in banking provides extraordinary capability. But without structured oversight, that capability can amplify vulnerabilities. The most mature institutions embed supervisory logic directly into their systems, ensuring that automation enhances rather than destabilizes performance.

Excellence, in this context, is not speed alone. It is governable speed.

Trust as Competitive Infrastructure

Trust in financial institutions has always mattered. In the age of artificial intelligence in banking, it becomes structural infrastructure. Supervisory confidence influences how quickly institutions can deploy new technologies and expand automation.

AI governance in financial services acts as a competitive differentiator. Banks that demonstrate disciplined oversight receive regulatory comfort earlier. They encounter fewer constraints when introducing advanced systems. Partnerships with fintech firms proceed more smoothly when institutional controls are clear.

Conversely, institutions perceived as less governable may face incremental approvals, model freezes during stress events, or heightened reporting obligations. Over time, this creates divergence. Trust determines operational flexibility.

Artificial intelligence in banking is abundant across the industry. Permission to scale it confidently is not. Trust shapes capital flows, supervisory relationships, and long-term strategic advantage.

In this environment, institutional design becomes a signal. The architecture of governance communicates stability before a crisis ever emerges.

Leadership and the Institutional Mandate

Digital transformation in the banking industry has traditionally been delegated to technology teams. Today, AI adoption in financial services requires board-level engagement. Leadership must define what can and cannot be automated, how systems are monitored, and where ethical boundaries lie.

AI governance in financial services is ultimately a leadership responsibility. Executives must ensure that intelligent systems reflect institutional values and risk appetite. They must be prepared to explain decisions under scrutiny and adjust frameworks as technology evolves.

Artificial intelligence in banking introduces moral and regulatory complexity. Leaders cannot treat intelligent systems as black boxes. They must understand how data is sourced, how models learn, and how bias is mitigated.

Institutional stewardship replaces operational micromanagement. The role of leadership is to design guardrails, maintain transparency, and ensure that innovation aligns with long-term credibility.

In an era of rapid transformation, trust rests not only on systems but on those who govern them.

The future of banking will not be decided by the smartest systems, but by the leaders who govern them responsibly

Conclusion: The Future Will Be Governed by Trust

Artificial intelligence in banking is redefining the technology in the banking industry and accelerating digital transformation in the banking industry. Yet intelligence alone does not secure institutional success.

Operational excellence in banking now depends on governance, explainability, and disciplined AI risk management in banking. Generative AI in banking will continue to unlock productivity, but its legitimacy depends on containment and oversight.

In this new landscape, intelligence is widespread. Trust is scarce. Institutions that embed AI governance in financial services at the core of their operating models will scale confidently. Those that neglect structural control will encounter friction.

The future of artificial intelligence in banking will not be decided by who builds the most sophisticated systems. It will be decided by who remains explainable, governable, and resilient at speed.

The institutions that endure will not simply be intelligent. They will be trusted.

Frequently Asked Questions (FAQs)

How is artificial intelligence used in banking?

Artificial intelligence in banking is used across core operational and customer-facing functions. Banks apply AI for credit risk assessment, fraud detection, anti-money laundering monitoring, customer service chatbots, predictive analytics, and regulatory compliance automation. AI also strengthens automation in banking operations by enabling real-time anomaly detection and decision-making. Increasingly, generative AI in banking is being used for document processing, customer communication drafting, and internal knowledge management. As part of the broader digital transformation in the banking industry, AI now functions as a decision-support and risk-control layer embedded into daily operations.

What are the five benefits of AI in banking?

The key benefits of artificial intelligence in banking include improved risk management, enhanced fraud detection, faster customer service, operational efficiency, and better data-driven decision-making. AI adoption in financial services allows banks to reduce manual errors while scaling automation in banking operations. AI also supports predictive analytics, helping institutions anticipate liquidity needs and credit risks more accurately. As digital transformation in the banking industry accelerates, AI enables smarter cost optimization and improved regulatory reporting, strengthening overall operational excellence in banking.

What are the disadvantages of AI in banks?

Despite its advantages, artificial intelligence in banking presents challenges. AI risk management in banking must address data bias, model opacity, cybersecurity risks, and over-reliance on automated systems. Generative AI in banking can introduce risks such as inaccurate outputs or data leakage if not properly governed. Without strong AI governance in financial services, intelligent systems may amplify operational vulnerabilities. Additionally, high implementation costs and regulatory scrutiny can slow adoption. Therefore, effective oversight and explainable AI in banking are critical to maintaining trust and compliance.

What is the future of AI in banking in 2026?

By 2026, artificial intelligence in banking is expected to become deeply integrated into core operating models rather than functioning as a standalone technology. Generative AI in banking will expand into advisory support, regulatory reporting, and personalized financial insights. AI governance in financial services will mature, with stronger regulatory frameworks and greater emphasis on explainable AI in banking. The future will likely see AI-native institutions leading the digital transformation in the banking industry, combining automation with structured oversight to achieve sustainable operational excellence in banking.

The future of AI in banking will not be defined by algorithms. It will be defined by whether institutions redesign governance fast enough to sustain public trust.